Sales Tax for Photographers: A Working Photographer's Guide to What You Owe and How to Stay Compliant

- austenhunter

- May 30

- 8 min read

Most photographers don't realize they owe sales tax — until a letter from their state's Department of Revenue shows up two years into running the business. By then it's back-taxes plus penalties plus interest on every session they ever shot, and the math gets ugly fast. A photographer doing $60,000 a year in untaxed sessions in a 6% sales-tax state can owe upwards of $7,000 in collectible-but-uncollected sales tax — before penalties.

I run Austen Hunter Photography, a portrait and headshot business alongside my full-time Navy Public Affairs career, and earned the 2024 Navy Civilian Photographer of the Year title along the way. Below is the working-photographer guide to sales tax: what most states tax, how to register and file, and the math behind getting it wrong. I'm not a CPA — this is the framework I run, but state rules vary and your specific situation needs a tax professional. The principles here will save you that consultation's worth of time.

Key Takeaways

|

Do Photographers Have to Charge Sales Tax?

Almost always — though the rules vary by state, by what you're selling, and by how you deliver it. The default assumption a working photographer should run with: yes, sales tax applies to your business unless you can document that it doesn't.

Three categories of photography revenue have different rules:

Tangible products (prints, albums, USB drives, framed images, gift prints) are taxable in almost every state. If you hand the client a physical thing, your state's general sales tax applies.

Photography services (the session fee itself, separate from any product) are taxable in roughly 25 states. Some states tax services broadly; some tax only services that result in a tangible product; some don't tax services at all. The Tax Foundation's state-by-state sales tax overview is the cleanest reference for what your state does.

Digital products (download links, online gallery delivery, cloud-only files) are the trickiest category. About 20 states now treat digital photography deliverables as taxable; others don't. This category has been expanding fast — a state that didn't tax digital delivery five years ago may now.

The rule: check your state's Department of Revenue (search "[your state] sales tax photographer" or "[your state] DoR sales tax services"). What you'll find is usually clearer than expected — most state DoR sites publish photographer-specific guidance because it's a common question.

"Photographers I've talked to who got caught by sales tax weren't avoiding it on purpose. They didn't know it applied to them, and the state didn't tell them until two years of back-taxes had stacked up." — Austen Hunter

Which Photography Services and Products Get Taxed (And Which Don't)

The framework most working photographers can use as a starting point — then verify against state rules:

Almost always taxable:

Printed photos delivered to client

Albums, books, frames, mounted images

USB drives, SD cards, or other physical media

Mini-sessions where the photographer also sells prints on-site

Often taxable (state-dependent):

Session fees with no product (portrait sittings, headshot sessions)

Digital gallery downloads

Travel fees billed separately

Setup fees for events

Rarely taxable (state-dependent):

Editorial work where the publication is the buyer (often resale-exempt)

Pure consultation or "scouting" sessions where no images are delivered

Sessions performed for tax-exempt nonprofits or government clients (the entity, not the photographer, is exempt)

How Sales Tax Rules Vary by State (And Why Yours Probably Matters Differently)

State variation is the part most state-by-state guides bury. The short version:

Service-tax states (services taxed regardless of product) include Hawaii, New Mexico, South Dakota, West Virginia, and parts of Washington. If you operate in one of these, your session fee itself is taxable — no debate.

Product-only tax states (services exempt; products taxed) include California, New York, Florida (with caveats), Illinois, and most others. The session fee is generally exempt, but anything tangible delivered is taxable.

Mixed states (services taxed only when "in connection with" a tangible product) include Texas, Pennsylvania, and several Southeast states. If your contract bundles the session and the prints together, the whole bundle is usually taxable. If you separate the session fee from a print order, only the print order is taxable.

The "bundling trap" in mixed states: if you charge one combined fee that includes both the session and any prints, the entire fee often becomes taxable — even the service portion that wouldn't be taxable on its own. The fix in mixed states is to invoice the session and the products as separate line items on the contract, so the tax authority sees them as distinct.

This is the area where a one-hour consultation with a state-specific CPA pays for itself fastest. The $200 you spend on the consultation can save thousands in back-taxes or in over-collected sales tax (which is also a problem — you can't just keep it).

How to Register, Collect, and File Photography Sales Tax

Three steps, in order, none of them as scary as they sound:

1. Register for a sales tax permit (or "seller's permit" / "resale certificate") in your state. Almost every state's Department of Revenue lets you register online in 15-30 minutes. The application asks for your business name, EIN (or SSN if sole proprietor), business address, and an estimate of your annual sales volume. Most states issue the permit in 1-3 days. There's no fee in most states; a handful charge $5-25.

The Small Business Administration's sales tax overview covers the federal context and links to each state's registration portal.

2. Collect sales tax on every taxable sale — as a separate line item. Don't bury the tax in the session price. Add it to the invoice clearly: "Session Fee: $1,200. Sales Tax (6%): $72. Total: $1,272." The client sees what they're being charged. You see what to remit. The state sees clean records.

The 6% example assumes Florida-style rates; your state's combined state + local rate may be 4% to 11%. Avalara's state sales tax rate lookup is the cleanest place to check.

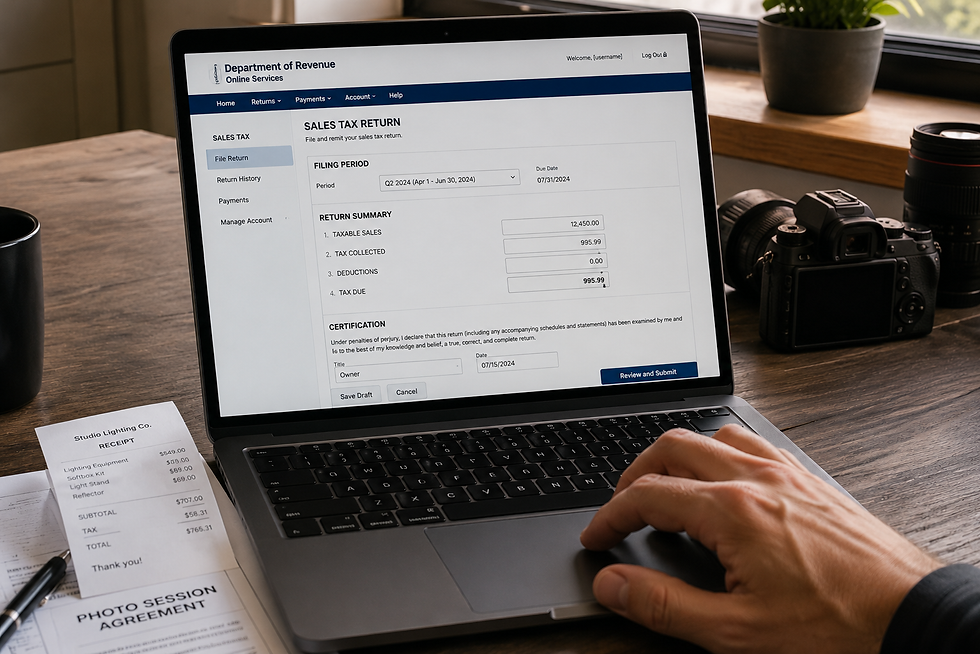

3. File and remit on your state's required cadence. Most states require monthly, quarterly, or annual filing based on your volume. New photography businesses are usually placed on annual or quarterly cadence; growing ones move to monthly. The state sends a notice telling you the cadence — follow what they assign.

Filing typically takes 15-30 minutes per period: log into your state's DoR portal, enter your total taxable sales, the tax collected, and remit. Most states accept ACH directly from your business bank account.

What Happens If You Don't Collect Sales Tax on Photography Sessions

The painful part. If your state determines you should have been collecting sales tax and didn't, you owe the sales tax yourself — out of pocket — for every past sale, even though you never collected it from the client.

"The state isn't trying to catch you on sales tax. They want you registered, filing, and remitting. The moment you self-correct, the conversation gets a lot easier." — Austen Hunter

Concrete example. A Florida-based photographer (6% combined rate) shoots 80 portrait sessions a year at an average of $800 each, plus $20,000 in print sales — total $84,000 in taxable revenue. Sales tax owed at 6%: about $5,040 per year. Two years uncollected = roughly $10,080 in back-tax exposure, before penalties (typically 10-25% of the owed amount) and interest (varies by state, usually 6-12% annually).

The state finds out one of three ways:

A 1099 you filed shows revenue but no corresponding sales tax remittance

A competitor reports you (this is more common than photographers realize)

A random audit flags the discrepancy

The fix isn't waiting it out. Most states have voluntary disclosure programs that let you self-report past uncollected sales tax in exchange for reduced or waived penalties. If you've been operating without collecting and you're worried, contact a CPA before the state contacts you. The penalty math is dramatically better when you come forward first.

Photography Sales Tax at a Glance

What you sell | Taxable in most states? | When to verify with your state |

Printed photos, albums, frames | Yes | Before your first product order |

USB/SD card delivery | Yes (tangible media) | Before your first delivery |

Session fee only (no product) | Sometimes (~25 states) | Before your first booking |

Digital gallery download | Sometimes (~20 states) | Before your first delivery |

Travel/mileage fees | Often follows session fee taxability | Before your first travel charge |

Editorial publication work | Often resale-exempt with proper certificate | Before your first editorial invoice |

This sits inside the broader framework for running a profitable photography business — alongside pricing strategy, the contracts that protect every session, and the copyright and insurance protections that live outside the contract.

How to Set Up a Photography Sales Tax System This Month

Three steps. Each takes under an hour.

This week: Go to your state's Department of Revenue website. Search "[your state] sales tax services" and "[your state] sales tax digital products." Document what your state taxes. Identify your effective rate (state + local combined).

Next week: Register for a sales tax permit through your state's DoR portal. 15-30 minutes online. Save the permit number and the filing cadence the state assigns.

The week after: Update your contract template to include a sales tax line. Update your invoicing system (Honeybook, Studio Ninja, QuickBooks, whatever you use) to add sales tax automatically on taxable line items. Test it on your next inquiry.

That's the entire setup. From "I don't know if I owe" to "I'm collecting and remitting correctly" in about three hours of work, spread across three weeks.

If you've been operating without collecting and you're worried about exposure, the next call to make is to a CPA who specializes in small-business or self-employed clients. The voluntary disclosure path is usually 70-90% cheaper than waiting to get caught.

If you are building a professional photography business, I can't stress how important it is to have a mentor. Getting proper feedback and guidance is a much more effecient way to grow than learning things the hard way. I run 60-minute 1:1 mentorship sessions covering the portrait techniques and business practices to help photographers level up their business. Book a mentorship session today and supercharge your business!

Frequently Asked Questions

Do photographers have to charge sales tax?

In most states, yes — at minimum on physical products like prints and albums. About 25 states also tax photography services. Check your state's Department of Revenue for the specific rules in your jurisdiction.

What's the difference between taxing services and taxing products in photography?

Tangible products (prints, albums, USB drives) are taxable in almost every state. Photography services (the session fee itself) are taxable in roughly 25 states — the rules vary widely, and "mixed" states tax services only when bundled with a product.

How do I register to collect sales tax as a photographer?

Go to your state's Department of Revenue website and register for a sales tax permit. The process takes 15-30 minutes online and the permit usually issues in 1-3 days. Most states don't charge a registration fee.

What happens if I never collected sales tax on photography sessions?

You owe the sales tax yourself for past taxable sales — out of pocket — plus penalties (10-25%) and interest. Most states have voluntary disclosure programs that reduce penalties if you self-report before the state finds out. Contact a CPA before contacting the state.

Should I show sales tax separately on photography invoices?

Yes. List sales tax as a clear line item on the invoice: "Session Fee: $1,200. Sales Tax (6%): $72. Total: $1,272." Don't bury it in the session price — the client should see what they're paying, and the state expects clean records.

Comments